e-Invoicing under GST denotes electronic invoicing defined by the GST law. Just like how a GST-registered business uses an e-way bill while transporting goods from one place to another. Similarly, certain notified GST-registered businesses must generate e invoice for Business-to-Business (B2B) transactions.

Clear is officially GSTN-approved IRP. More than 3,000 large enterprises trust the Clear e-Invoicing solution for unified e-invoicing and e-way bill compliance journey. We provide the best-in-class e-invoicing solution for businesses of any scale and industry. Do not miss exploring the Clear e-Invoicing solution!

Latest Updates

12th June 2023

The NIC has made it mandatory for taxpayers with turnover more than Rs.100 Crore to login using the Two-factor Authentication from 15th July 2023 for both the e-invoicing and e-way bill systems.

9th June 2023

The GSTN has launched an ‘e-Invoice QR Code Verifier’ app on Google Play Store to enable users to quickly and conveniently verify e-invoices. The user-friendly app will authenticate the information embedded in the QR code, which can be compared with the information printed on the e-invoice. The iOS version will be available shortly.

10th May 2023

CBIC notified the 6th phase of e-invoicing. Hence, taxpayers with ₹5 Cr+ turnover in any financial year from 2017-18 shall issue e-invoices w.e.f 1st August 2023.

6th May 2023

The GST department has deferred the time limit of 7 days to report the old e-invoices on the e-invoice IRP portals by three months. Further, the department is yet to announce the new implementation date.

‘e-Invoicing’ or ‘electronic invoicing’ is a system in which B2B invoices and a few other documents are authenticated electronically by GSTN for further use on the common GST portal.

In its 35th meeting, the GST Council decided to implement a system of e-Invoicing, covering specific categories of persons, mostly large enterprises. Later on, it has been expanded to cover mid-sized businesses and small businesses as well.

e-Invoicing does not imply the generation of invoices on the GST portal but it means submitting an already generated standard invoice on a common e invoice portal. Thus, it automates multi-purpose reporting with a one-time input of invoice details. The CBIC notified a set of common portals to prepare e invoice via Notification No.69/2019 – Central Tax.

Under the electronic invoicing system, an identification number will be issued against every invoice by the Invoice Registration Portal (IRP), managed by the GST Network (GSTN). The National Informatics Centre launched the first IRP at einvoice1.gst.gov.in.

All invoice information gets transferred from this portal to both the GST portal and the e-way bill portal in real-time. Therefore, it eliminates the need for manual data entry while filing GSTR-1 returns and generation of part-A of the e-way bills, as the information is passed directly by the IRP to the GST portal.

The e invoice applicability can be explained as follows-

Turnover criteria or e Invoice limit

| Phase | Applicable to taxpayers having an aggregate turnover of more than | Applicable date | Notification number |

| I | Rs 500 crore | 01.10.2020 | 61/2020 – Central Tax and 70/2020 – Central Tax |

| II | Rs 100 crore | 01.01.2021 | 88/2020 – Central Tax |

| III | Rs 50 crore | 01.04.2021 | 5/2021 – Central Tax |

| IV | Rs 20 crore | 01.04.2022 | 1/2022 – Central Tax |

| V | Rs 10 crore | 01.10.2022 | 17/2022 – Central Tax |

| VI | Rs 5 crore | 01.08.2023 | 10/2023 - Central Tax |

The taxpayers must comply with e-invoicing in FY 2022-23 and onwards if their e invoice limit or turnover exceeds the specified limit in any financial year from 2017-18 to 2021-22. Also, the aggregate turnover will include the turnover of all GSTINs under a single PAN across India.

If the turnover in the last FY was below the threshold limit but it increased beyond the threshold limit in the current year, then e-Invoicing would apply from the beginning of the next financial year i.e. FY 2023-24.

Suppose, ABC ltd aggregate turnover was as follows-

FY 2017-18: Rs 15 crore

FY 2018-19: Rs 17 crore

FY 2019-20: Rs 24 crore

FY 2020-21: Rs 19 crore

FY 2021-22: Rs 18 crore

Suppose, QPR ltd started business in FY 2019-20 and earned aggregate turnover as follows-

FY 2019-20: Rs 4 crore

FY 2020-21: Rs 7 crore

FY 2021-22: Rs 11 crore

The ABC Ltd shall mandatorily generate e invoices from 01.04.2022 irrespective of the current year’s aggregate turnover as it has crossed the Rs 20 crore turnover limit in FY 2019-20.

On the other hand, QPR ltd should comply with e-Invoicing from 1st October 2022 since its previous year’s annual turnover exceeds Rs.10 crore.

The fifth phase of e-Invoicing works similar to the fourth phase. Watch the below video to learn easily.

Transactions and documents criteria

The following transactions and documents listed below fall under

e invoicing applicability –

| Documents | Transactions |

| Tax invoices, credit notes and debit notes under Section 34 of the CGST Act | Taxable Business-to-Business sale of goods or services, Business-to-government sale of goods or services, exports, deemed exports, supplies to SEZ (with or without tax payment), stock transfers or supply of services to distinct persons, SEZ developers, and supplies under reverse charge covered by Section 9(3) of the CGST Act. |

However, irrespective of the turnover, e-Invoicing shall not be applicable to the following categories of registered persons for now, as notified in CBIC Notification No.13/2020 – Central Tax, amended from time to time-

| Notified Businesses | Documents | Transactions |

| 1)An insurer or a banking company or a financial institution, including an NBFC 2) A Goods Transport Agency (GTA) 3) A registered person supplying passenger transportation services 4) A registered person supplying services by way of admission to the exhibition of cinematographic films in multiplex services 5) An SEZ unit (excluded via CBIC Notification No. 61/2020 – Central Tax) 6) A government department and Local authority (excluded via CBIC Notification No. 23/2021 – Central Tax) 7) Persons registered in terms of Rule 14 of CGST Rules (OIDAR) | Delivery challans, Bill of supply, financial or commercial credit note or debit note, bill of entry, and ISD invoices. | Any Business-to-Consumers (B2C) sales, Nil-rated or non-taxable or exempt B2B sale of goods or services, nil-rated or non-taxable or exempt B2G sale of goods or services, imports, high sea sales and bonded warehouse sales, Free Trade & Warehousing Zones (FTWZ), and supplies under reverse charge covered by Section 9(4) of the CGST Act. |

Before e-invoicing could apply, businesses generated invoices through various software, and the details of these invoices were manually uploaded in the GSTR-1 return or using ERP.

Once the respective suppliers file the GSTR-1, the invoice information gets reflected in GSTR-2B for the recipients. On the other hand, the consignor or transporters had to generate e-way bills by again importing the invoices in Excel or JSON manually or via ERP.

Under the e-invoicing system, the process of generating and uploading invoice details will remain the same. It’s done by importing using the Excel tool/JSON or via API integration, either directly or through a GST Suvidha Provider (GSP). The data will seamlessly flow for GSTR-1 preparation and for the e-way bill generation too. The e-invoicing system will be the key tool to enable this.

Until 30th April 2023, there has been no time limit fixed by the GST systems or the GST law to generate e-invoices. From 1st May 2023* onwards, taxpayers with Annual Aggregate Turnover (AATO) equal to or more than INR 100 crore must generate e-invoices for tax invoices and credit-debit notes within 7 days of invoice date, failing which such invoices and CDNs will be considered non-compliant.

Further, there is no defined time limit or period within which e invoice must be generated for the rest of the applicable taxpayers. Therefore, such taxpayers are advised to create e invoice on or after the invoice/CDN date preferably a week before the filing of GSTR-1 returns since it takes T+3 days for details of e-invoices to get auto-populated into GSTR-1.

* However, on 6th May 2023, the department has deferred the time limit of 7 days to report the old e-invoices on the IRP portals by three months. Also, the department is yet to announce the new implementation date.

The following are the stages involved in generating or raising an e-invoice.

A taxpayer can continue to print his invoice as being done presently with a logo. The e-invoicing system only mandates all taxpayers to report invoices on IRP in electronic format.

Businesses will have the following benefits by using e-invoice initiated by GSTN-

It will help in curbing tax evasion in the following ways-

e-Invoice must primarily adhere to the GST invoicing rules. Apart from this, it should also accommodate the invoicing system or policies followed by each industry or sector in India. Certain information is made mandatory, whereas the rest of it is optional for businesses. Many fields are also made optional, and users can choose to fill up relevant fields only. It has also described every field along with the sample inputs for the interested users. One can see that certain required fields from the e-way bill format are included now in the e-invoice, such as the sub-supply type.

Below is the gist of the contents of the latest e-invoice format as notified on 30th July 2020 via Notification No.60/2020 – Central Tax:

The following fields must be compulsorily be declared in an e-invoice:

| Sl. no. | Name of the field | List of choices/ specifications/sample Inputs | Remarks |

| 1 | Document Type Code | Enumerated List such as INV/CRN/DBN | Type of document must be specified |

| 2 | Supplier_Legal Name | String Max length: 100 | Legal name of the supplier must be as per the PAN card |

| 3 | Supplier_GSTIN | Max length: 15 Must be alphanumeric | GSTIN of the supplier raising the e-invoice |

| 4 | Supplier_Address | Max length: 100 | Building/Flat no., Road/Street, Locality, etc. of the supplier raising the e-invoice |

| 5 | Supplier_Place | Max length: 50 | Supplier’s location such as city/town/village must be mentioned |

| 6 | Supplier_State_Code | Enumerated list of states | The state must be selected from the latest list given by GSTN |

| 7 | Supplier Pincode | Six digit code | The place (locality/district/state) of the supplier’s locality |

| 8 | Document Number | Max length: 16 Sample can be “ Sa/1/2019” | For unique identification of the invoice, a sequential number is required within the business context, time frame, operating systems and records of the supplier. No identification scheme is to be used. |

| 9 | Preceeding_Invoice_Reference and date | Max length:16 Sample input is “ Sa/1/2019” and “16/11/2020” | Detail of original invoice which is being amended by a subsequent document such as a debit and credit note. It is required to keep future expansion of e-versions of credit notes, debit notes and other documents required under GST. |

| 10 | Document Date | String (DD/MM/YYYY) as per the technical field specification | The date when the invoice was issued. However, the format under explanatory notes refers to ‘YYYY-MM-DD’. Further clarity will be required. Document period start and end date must also be specified if selected. |

| 11 | Recipient_ Legal Name | Max length: 100 | The name of the buyer as per the PAN |

| 12 | Recipient’s GSTIN | Max length: 15 | The GSTIN of the buyer to be declared here |

| 13 | Recipient’s Address | Max length: 100 | Building/flat no., road/street, locality, etc. of the supplier raising the e-invoice |

| 14 | Recipient’s State Code | Enumerated list | The place of supply state code to be selected here |

| 15 | Place_Of_Supply_State_ Code | Enumerated list of states | The state must be selected from the latest list given by GSTN |

| 16 | Pincode | Six digit code | The place (locality/district/state) of the buyer on whom the invoice is raised/ billed to must be declared here if any |

| 17 | Recipient Place | Max length: 100 | Recipient’s location (City/Town/Village) |

| 18 | IRN- Invoice Reference Number | Max length: 64 Sample is ‘a5c12dca8 0e7433217…ba4013 750f2046f229’ | At the time of the registration request, this field is left empty by the supplier. Later on, a unique number will be generated by GSTN after uploading the e-invoice on the GSTN portal. An acknowledgement will be sent back to the supplier after the successful acceptance of the e-invoice by the portal. IRN should then be displayed on the e-invoice before use. |

| 19 | ShippingTo_GSTIN | Max length: 15 | GSTIN of the buyer himself or the person to whom the particular item is being delivered to |

| 20 | Shipping To_State, Pincode and State code | Max length: 100 for state, 6 digit pincode and enumerated list for code | State pertaining to the place to which the goods and services invoiced were or are delivered |

| 21 | Dispatch From_ Name, Address, Place and Pincode | Max length: 100 each and 6 digit for pincode | Entity’s details (name, and city/town/village) from where goods are dispatched |

| 22 | Is_Service | String (Length: 1) by selecting Y/N | Whether or not supply of service must be mentioned |

| 23 | Supply Type Code | Enumerated list of codes Sample values can be either of B2B/B2C/ SEZWP/S EZWOP/E XP WP/EXP WOP/DE XP | Code will be used to identify types of supply such as business to business, business to consumer, supply to SEZ/exports with or without payment, and deemed export. |

| 24 | Item Description | Max length: 300 The sample value is ‘Mobile’ The schema document refers to this as the ‘identification scheme identifier of the Item classification identifier’ | Simply put, the relevant description is generally used for the item in the trade. However, more clarity is needed on how it needs to be described for every two or more items belonging to the same HSN code. |

| 25 | HSN Code | Max length: 8 | The applicable HSN code for particular goods/service must be entered |

| 26 | Item_Price | Decimal (12,3) Sample value is ‘50’ | The unit price, exclusive of GST, before subtracting item price discount, can not be negative |

| 27 | Assessable Value | Decimal (13,2) Sample value is ‘5000’ | The price of an item, exclusive of GST, after subtracting the item price discount. Hence, gross price (-) discount = net price item, if any cash discount is provided at the time of sale |

| 28 | GST Rate | Decimal (3,2) Sample value is ‘5’ | The GST rate represented as a percentage that is applicable to the item being invoiced |

| 29 | IGST Value, CGST Value and SGST Value Separately | Decimal (11,2) Sample value is ‘650.00’ | For each individual item, IGST, CGST and SGST amounts have to be specified |

| 30 | Total Invoice Value | Decimal (11,2) | The total amount of the Invoice with GST. Must be rounded to a maximum of 2 decimals |

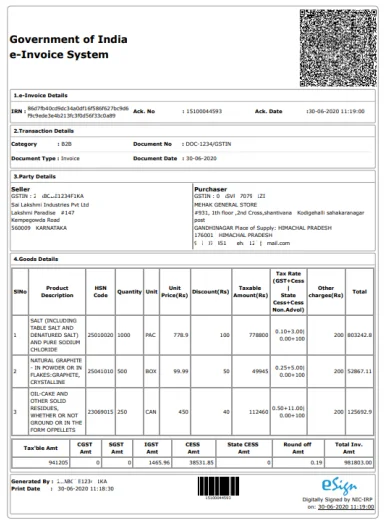

The e-invoice format notified is as follows:

Check out the detailed format of an e-invoice

Team Clear provides the best-in-class e-invoicing solution for businesses. The Clear e-invoicing solution also provides an e-Invoicing Tally Connector, enabling taxpayers to perform e-invoicing activities without leaving a tally screen. Team Clear ensures a safe migration to an upgraded UI with no changes to your historical data.

Team Clear also offers various modes through which e-invoices can be generated by the taxpayers, such as seamless API integrations, Excel mode, FTP, SFTP or Tally connector. The user can enjoy numerous value additions such as-

E-invoicing applies to GST registered persons whose aggregate turnover in any previous financial years (2017-18 to 2021-22) exceeded Rs.20 crore . From 1st August 2023, it applies to those with a turnover of more than Rs.5 crore up to Rs.10 crore . There are exceptions as listed in the above section.

Can an e-invoice be cancelled partially/fully?An e-invoice cannot be cancelled partially but can be cancelled wholly. On cancellation, it must be reported to the IRN within 24 hours. Any attempt to cancel thereafter cannot be done on the IRN and must be manually cancelled on the GST portal before the returns are filed.

Will the bulk uploading of invoices for the generation of IRN be possible?No, invoices must be uploaded one at a time into the IRP. The ERP of a business will need to be designed to place the request for the upload of individual invoices.

Will there be a facility for e-invoice generation on the common GST portal?No, invoices will continue to be generated on the individual ERP software currently in use by businesses. The invoice must adhere to the e-invoicing standard format and include the mandatory parameters. The direct generation of invoices on a common portal is not being planned at the moment.

What are the types of documents that are to be reported to the IRP?Invoices by the supplier, credit notes, debit notes as per the GST law, or any other document as notified under GST law are to be reported as an e-invoice.

For more FAQs on e-Invoicing, read our article on e-Invoicing FAQs .